On June 30, 2026, the Fifth Committee changed the 75-year-old rule that required the return of uncollected cash. This note explains the new credit-return methodology adopted by the General Assembly on a four-year trial basis. It does not address the broader peacekeeping financing crisis or the case for further reform. For that argument, see How to End the United Nations’ Current Financial Crisis… and Prevent Future Ones, which first set out the case for reforming this mechanism, and UN Peace Operations Gone Broke, which sets out the operational stakes this mechanism is meant to address.

The new methodology applies in the same way to the regular budget, peacekeeping budgets, and the international tribunals.

The reform does not change how credits are calculated or member states’ entitlement to them. It changes how and when those credits are returned.

What is a credit?

At the end of each financial period, actual expenditure is compared with the budget approved by the General Assembly. If expenditure is lower than the approved budget, the difference becomes a credit due to member states. That credit is then apportioned among member states according to the applicable scale of assessment.

Why was a change needed?

Under the previous methodology, credits were returned regardless of whether the Organization had actually collected the cash behind them. A member state that owed money could still receive a credit calculated against a budget the Organization had no cash to cover. The Board of Auditors called the result a “potentially dangerous spiral:” non-payment forces underspending, underspending generates credits, and returning those credits drains the cash the Organization needs the following year.

The previous methodology assumed that approved budgets would normally be fully financed. As persistent non-payment became more common, that assumption no longer held.

What changed?

The revised methodology changes the conditions under which credits are returned.

The objective is operational, not punitive: avoid returning cash the Organization has not yet received, while preserving every member state’s entitlement to its full share of any credit.

How the process works

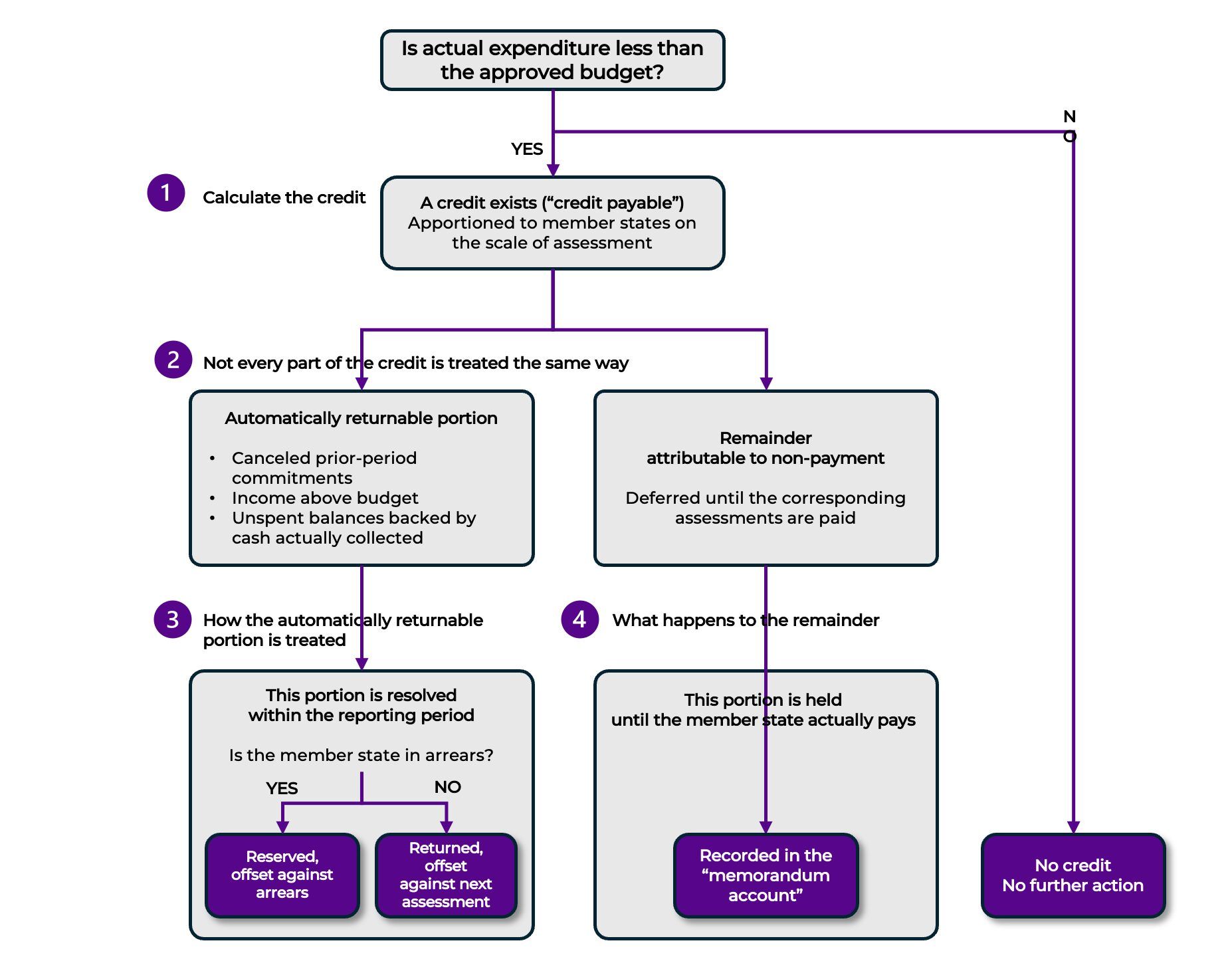

Step 1: Calculate the credit

The first step is unchanged. The Organization calculates the total credit by comparing the approved budget with actual expenditure. That total credit is then apportioned among member states according to the applicable scale of assessment. The resolution refers to this amount as the “credit payable.”

Step 2: Not every part of the credit is treated the same way

The methodology then separates the credit into two parts: one that qualifies for automatic return and one that is deferred until the corresponding assessments have been paid. The first part is the automatically returnable portion; it comprises three categories:

- Canceled prior-period commitments: money set aside for something that no longer needs to happen.

- Income received above what was budgeted.

- Unspent balances backed by cash actually collected for that year’s assessment.

Step 3: How the automatically returnable portion is treated

The automatically returnable portion is then treated as follows. If the member state is in arrears, the credit is offset against those arrears. If not, it is returned, offset against the member state’s next assessment. Either way, this portion is resolved within the reporting period.

Step 4: What happens to the remainder

The remaining portion of the credit is the portion attributable to non-payment. It is not canceled nor returned immediately. It is recorded in the member state’s “memorandum account”* and held until the corresponding assessment is paid.

The methodology also requires:

- Separate memorandum accounts for the regular budget, peacekeeping operations, and the international tribunals;

- Separate reporting of non-payment arising from external financial constraints, distinguished from non-payment arising from external financial constraints (including political decision not to pay).

Figure 1. Decision tree: How the credit methodology works